All the sales and purchases that take place in the world need to be recorded and accounted for, by both the seller and the buyer. That is an amazing thought, as billions and billions of transactions happen every day. Accountants and bookkeepers are needed to make sure these transactions are recorded properly, and that the information in the transactions can be organised in a sensible way.

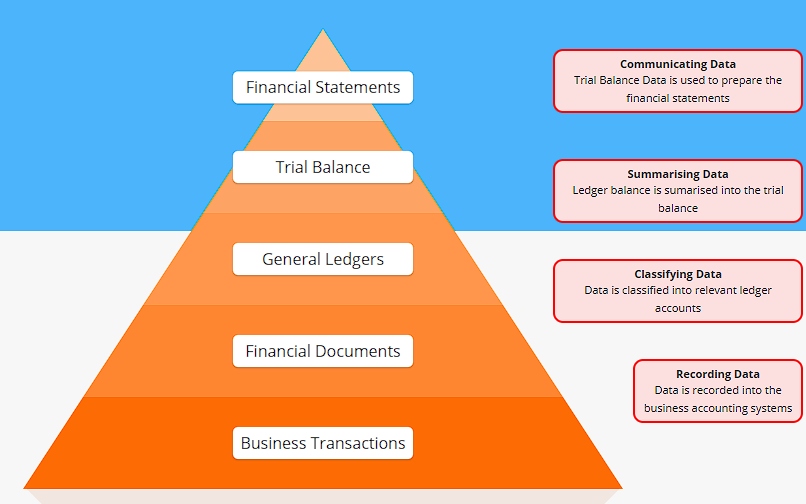

We have created an overview diagram that we call the Master Plan – it shows the process that we follow, from a transaction taking place, through to the financial statements. We look at how individual transactions are recorded, and how we can organise and summarise the key information about the transaction, so that we can produce financial statements at the end that tell us something useful about the performance of the business over the period.

Business Transactions

Business transactions are the business’s day-to-day activities that have a monetary value. For a business to operate, it needs to generate income by making sales and incur expenses such as purchases and overheads. All business transactions must be recorded in the accounting system with sufficient detail to enable the correct categorisation of the transaction for the purpose of preparing financial statements. Many transactions may be recorded automatically by computerised accounting systems – for example, in a retail store, as barcodes on the products are scanned at checkout, details of sales and inventory movements are automatically recorded.

Financial Documents

A financial document is produced for each business transaction to record information about individual transactions. Sales, purchases, cash payments and receipts are business transactions. Their corresponding documents are the sales invoice, purchase invoices, cheque stubs and remittance advice, respectively. Financial documents in a computerised system may be automatically generated as transactions are processed; controls will be implemented that make the source document’s creation, distribution, and authorisation mandatory before any transaction is recorded.

General Ledgers

The general ledger contains all the ledger accounts used by a business for the purpose of producing the financial statements. Information from the source documents is classified into their respective ledger accounts using double entries via computerised systems and manual journal entries. The general ledger contains seperate accounts for the business’s assets, liabilities, capital, income and expenses.

Trial Balance

Each ledger account balance is closed off, and the account balance flows to the trial balance. The trial balance is a list of each ledger account’s closing balances. An accountant prepares the trial balance periodically, usually once during year-end. If the information entered into the ledgers conforms to the principals of double-entry bookkeeping, the trial balance should have equal debit and credit balances. The trial balance is investigated to ensure no errors have occurred in recording the transactions.

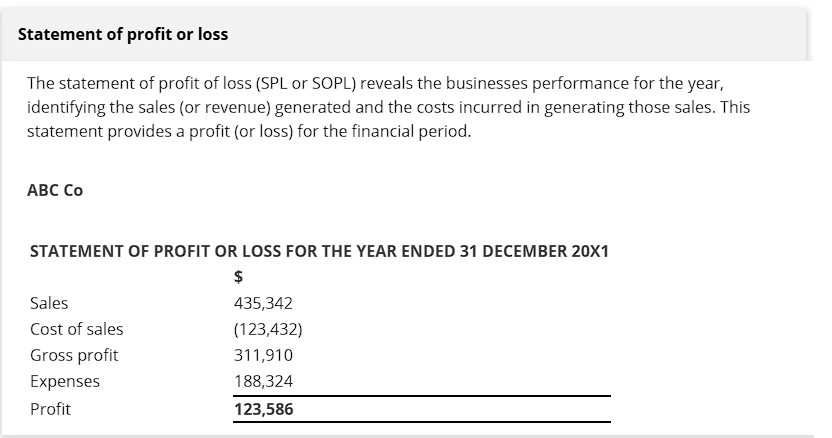

Financial Statements

Each ledger account balance in the trial balance is totalled and summarised into financial statement categories: assets, liabilities, capital, income or expenses. The statement of financial position provides an overview of a business’s assets, liabilities, and capital at the financial year-end. The statement of profit or loss summarises a business’s income and expenses during the financial year. The profit or loss is the net of the business’s income and expenses